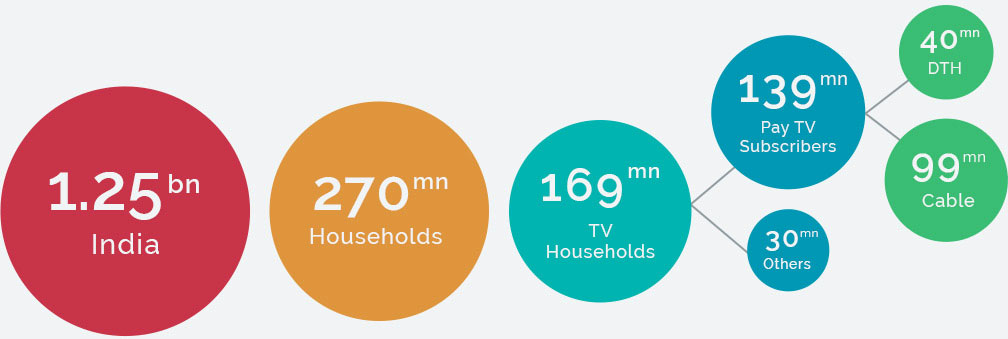

Impact of Digitization

Digitisation will benefit all stakeholders including consumers, the broadcasting industry, the distribution industry and the government. Consumers will benefit through an easy access to hundreds of new channels, sharper picture quality, better services and customised channel packages based on their individual preferences.

Consumers

Consumers will benefit through an easy access to hundreds of new channels, sharper picture quality, better services and customised channel packages based on their individual preferences.

The broadcasting sector

The broadcasting sector will benefit through higher transparency, resulting in lesser revenue leakages, more accurate subscriber base information and higher subscription revenues.

The distribution sector

The distribution sector will benefit from higher subscription revenues, more efficiencies, better margins, opportunity to sell bundled services and more accurate data collection.

The Government

The Government will benefit through higher transparency resulting in higher tax revenues. This has been a key reason for the rapid growth of the Direct-To-Home (DTH) business.